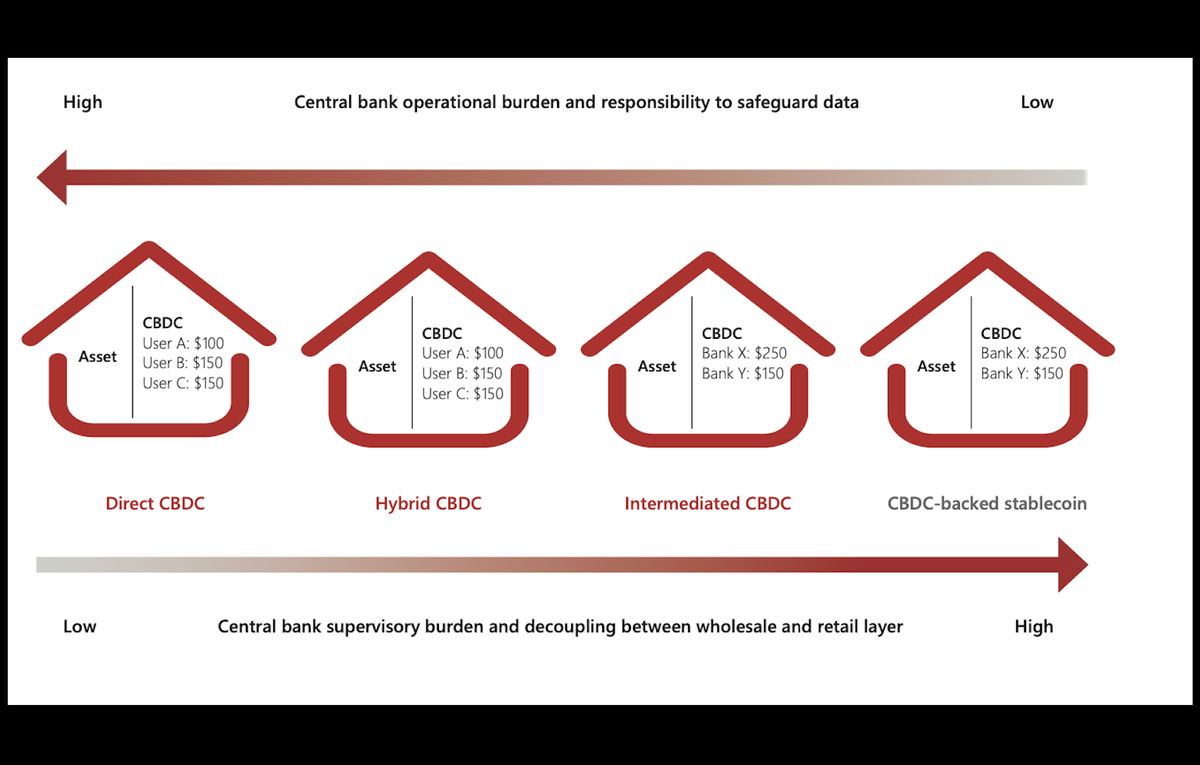

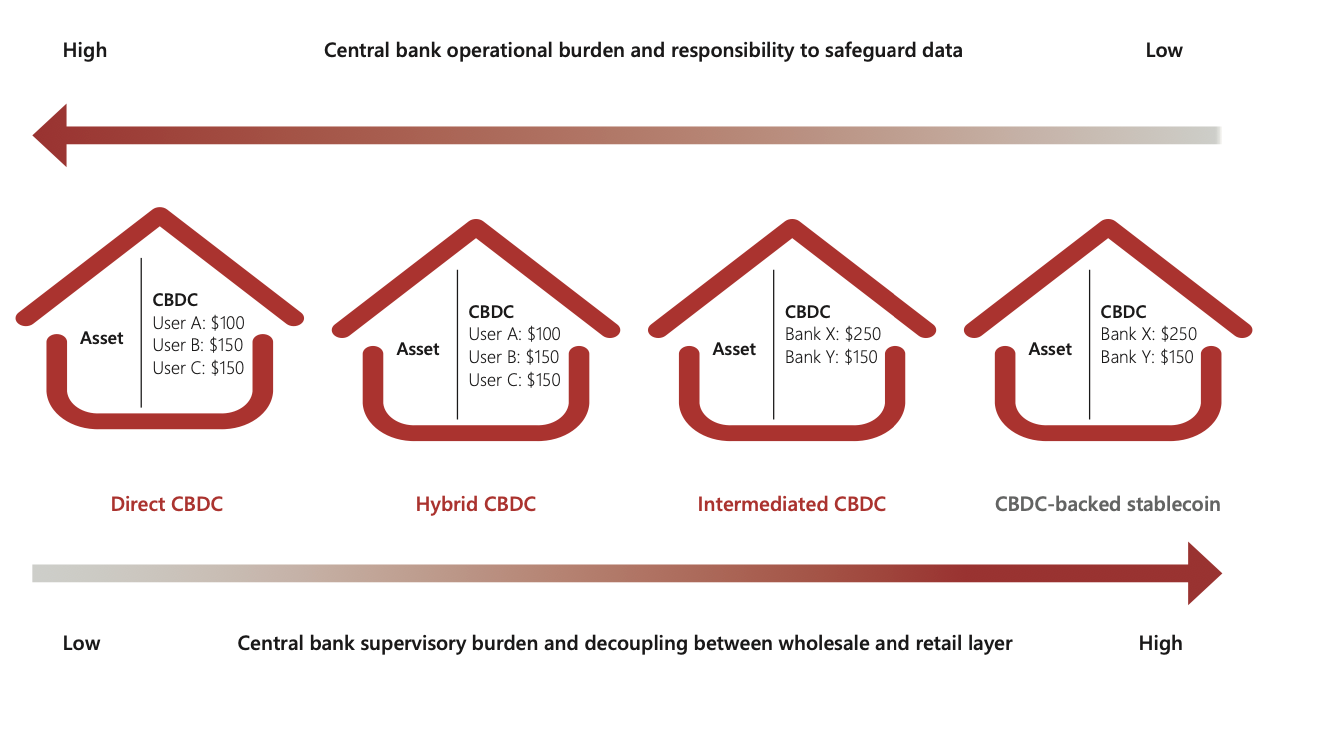

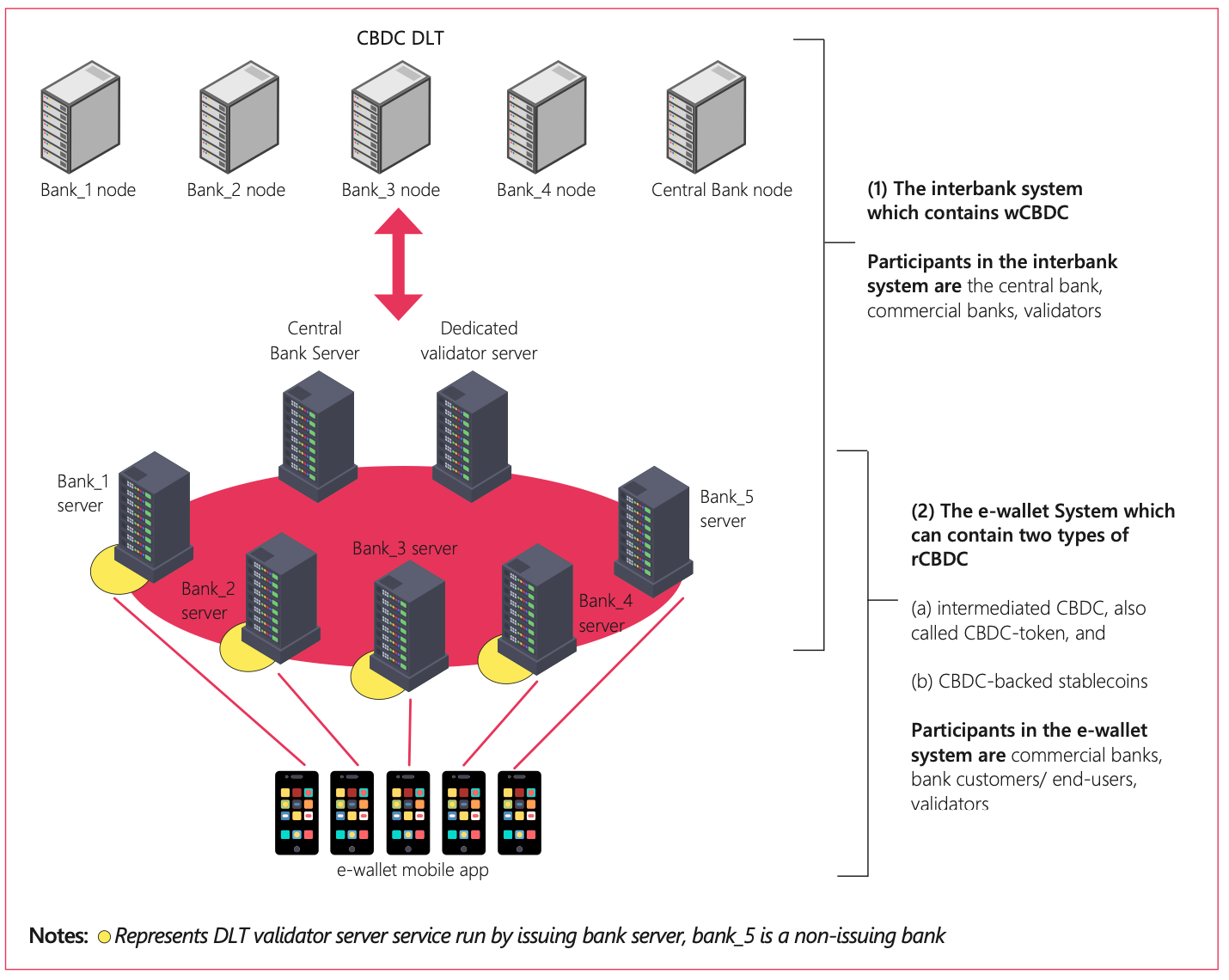

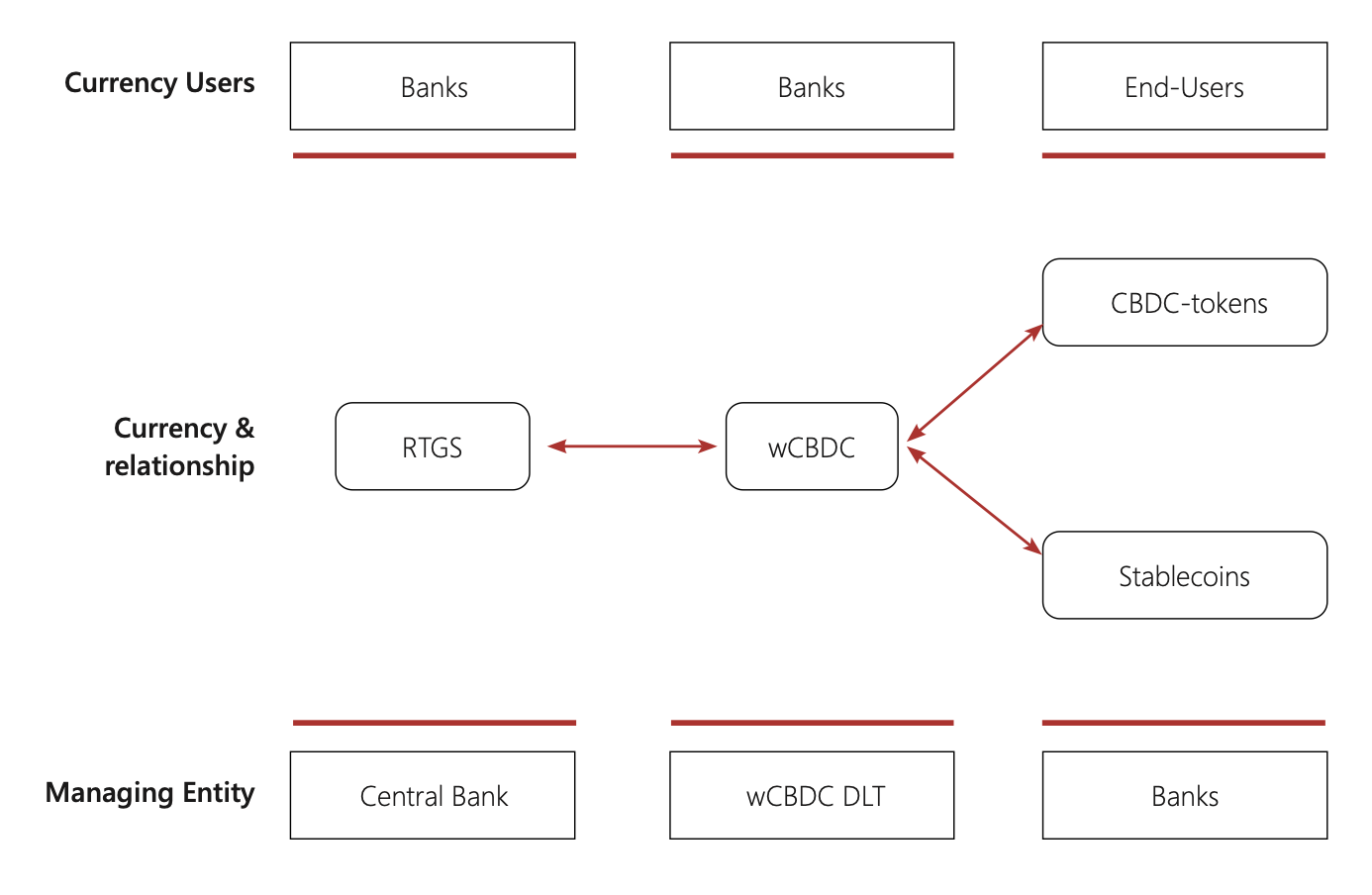

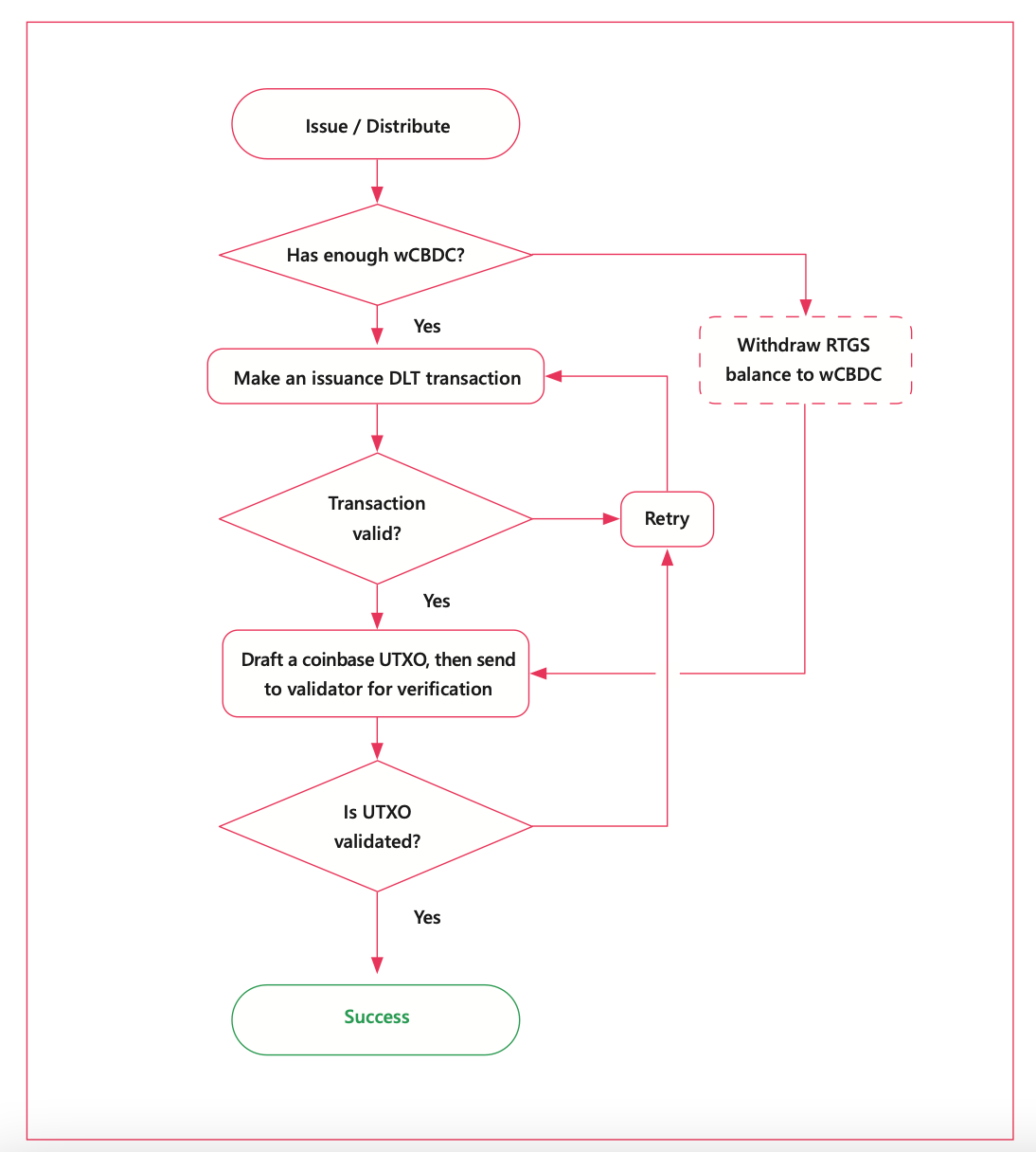

Hong Kong CBDC System Prototype Aurum

The Bank for International Settlements Innovation Hub Hong Kong Centre and the Hong Kong Monetary Authority cooperated to create a two-tier CBDC system that mirrors the current Hong Kong currency system and features unusual CBDC-backed stablecoins.