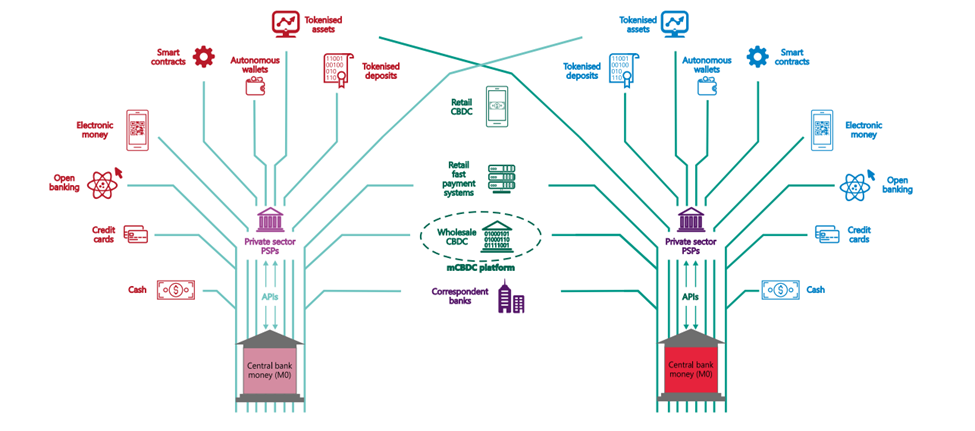

The Future Monetary System From BIS

BIS devoted one third of its 2022 Annual Economic Report for the discussion of the Future Monetary System. In their vision, Central Banks will have the core role, adopting innovations of DLT, leading and supervising the ecosystem of banks, PSP and other participants.