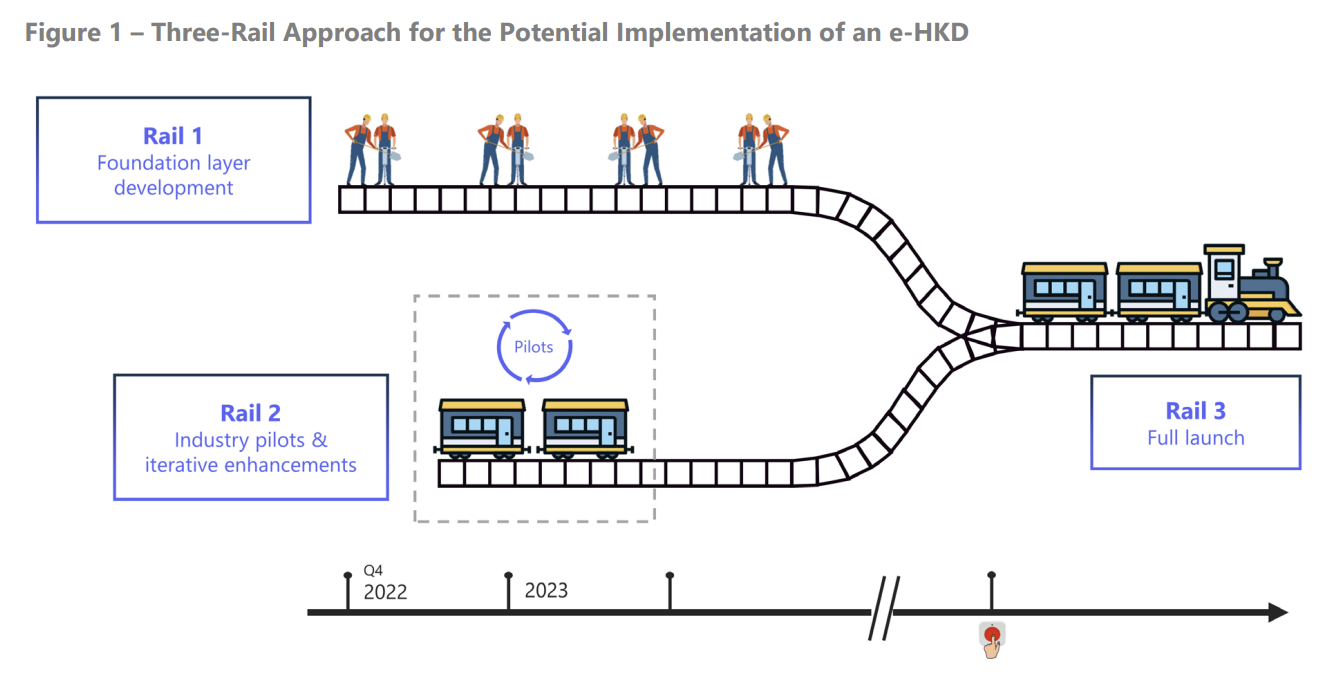

Hong Kong in Phase 2 of e-HKD Digital Dollar Pilot

The HKMA is taking its exploration of a digital Hong Kong dollar (e-HKD) to the next level. Phase 2 of the e-HKD Pilot Programme is now open for applications, inviting businesses to propose creative ways to utilize this digital currency.