Australia Central Bank Publishes Findings Of Its Digital Dollar Research Project

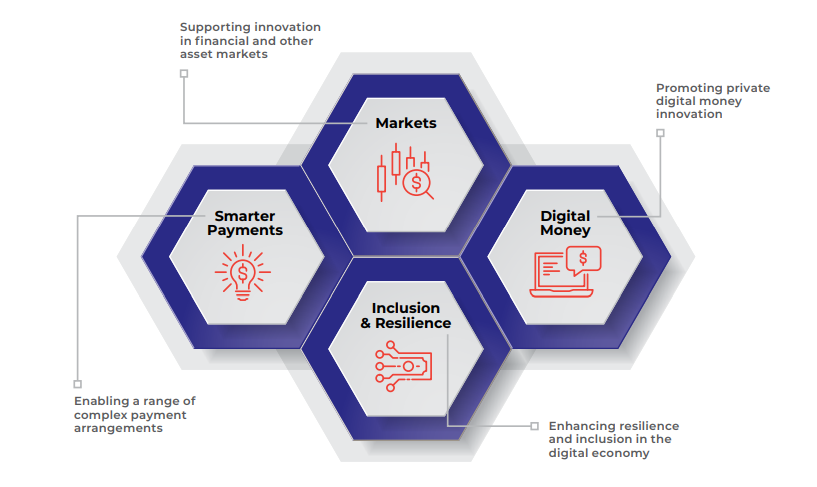

The Australian Central Bank Digital Currency Pilot was focused on exploring potential use cases with an aim to define the 'public policy rationale' for it. Four key themes were identified.