"Too Fat to Fly": Bitcoin Magazine CFO Warns of Bitcoin's Extinction

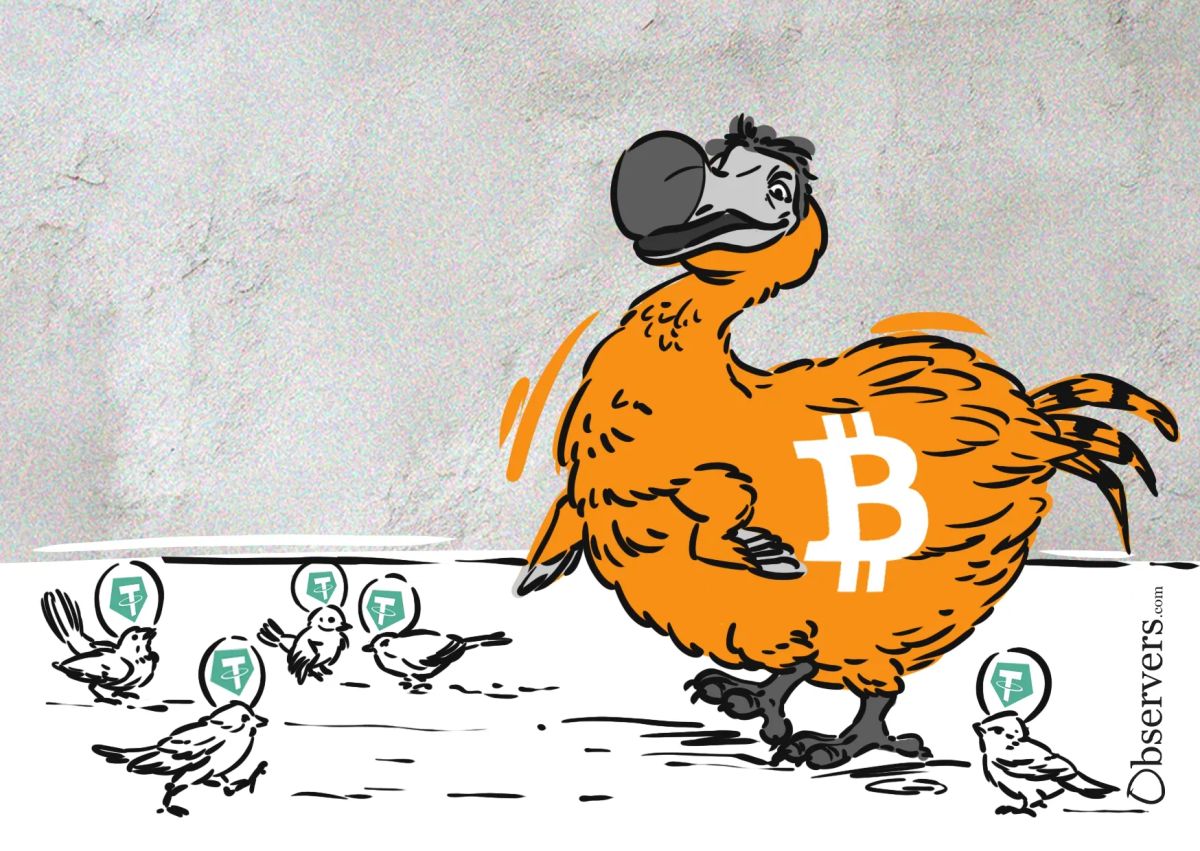

Di Lewis argues that its failure to evolve as a medium of exchange threatens its existence in the face of stablecoins, institutional ownership, and resistance to progress.

Di Lewis argues that its failure to evolve as a medium of exchange threatens its existence in the face of stablecoins, institutional ownership, and resistance to progress.