The Collapse of the Naira has Pushed Nigerians Towards Cryptocurrency

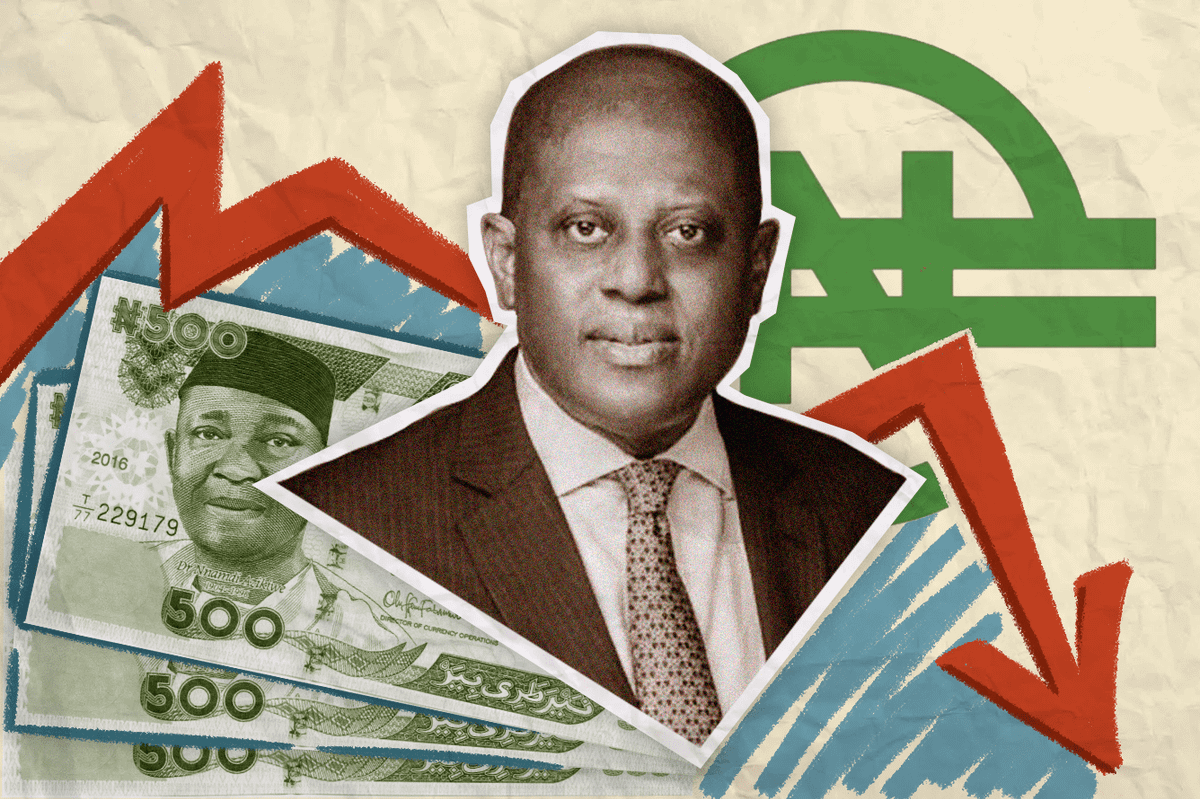

Since the new exchange rate kicked in, Nigeria’s national currency has fallen to a record low, leading people to find payment alternatives through crypto.

Since the new exchange rate kicked in, Nigeria’s national currency has fallen to a record low, leading people to find payment alternatives through crypto.