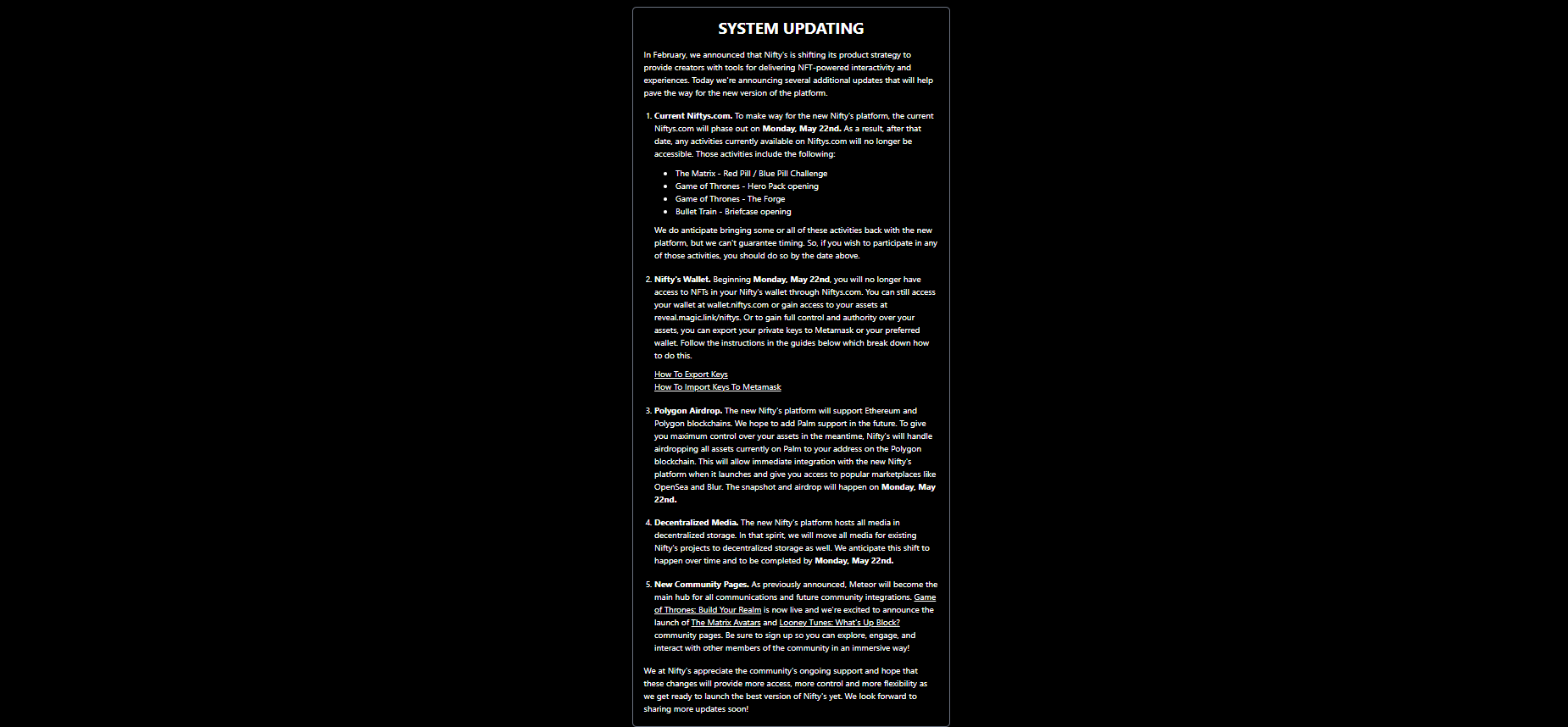

Nifty Marketplace Shuts Down: Is the NFT Industry Collapsing or Maturing?

Nifty, the NFT marketplace that released some of the most pop culture collections so far, has shut down. Is this a sign of the collapse of the NFT industry or of it reaching maturity?

:format(webp)/cdn.vox-cdn.com/uploads/chorus_asset/file/22714024/niftys_space_jam_nft.jpg)