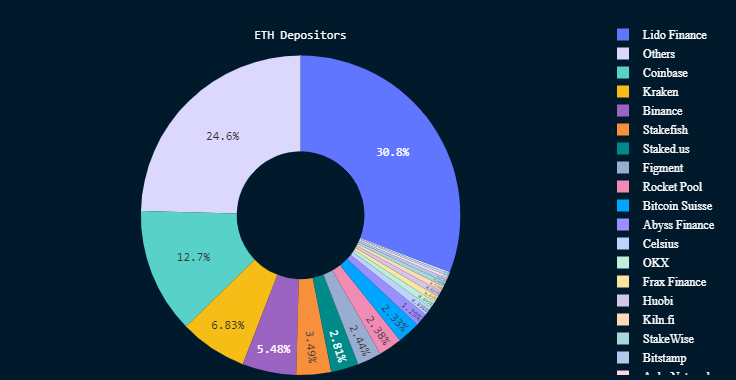

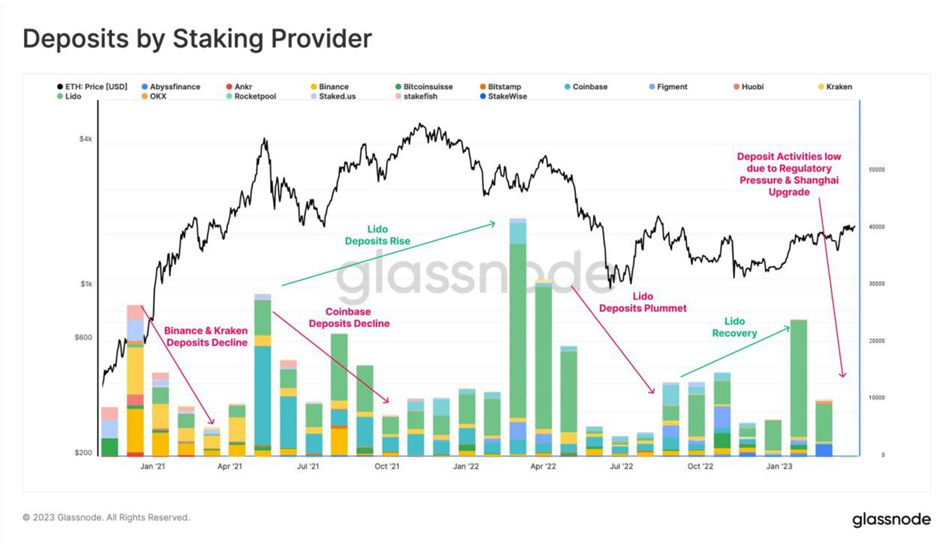

Ethereum Staking Markets Heat Up With Shapella Upgrade. Lido in Spotlight

Ethereum Shapella upgrade made staking on the largest blockchain financially more attractive and reignited competition in the staking-as-a-service business. Lido, a staking platform that provided a workaround before, can either lose or win it all.