USDC’s Circle Showcases Post-IPO Strength, Building Its Own Blockchain and Payment Networks

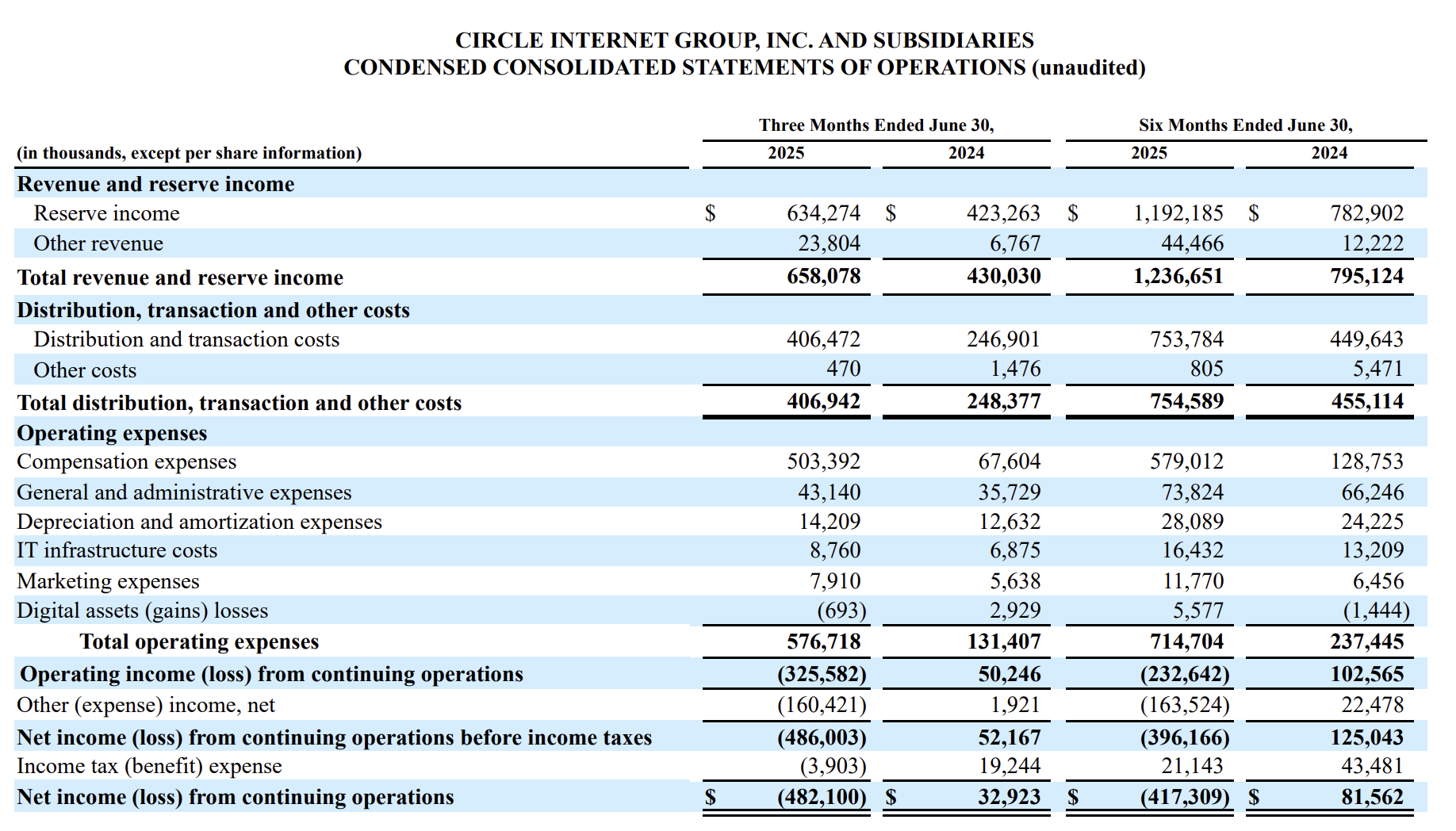

Circle’s first post-IPO results show USDC supply nearly doubled YoY to $61.3B, market share up to 26%, and revenue +53% to $658M. The $1.2B IPO boosted equity to $2.37B, funding new plays like the Circle Payments Network and Arc blockchain in a bid to challenge Tether’s dominance