Michael Saylor’s Second Bubble: From Dotcom Crash to Bitcoin Frenzy

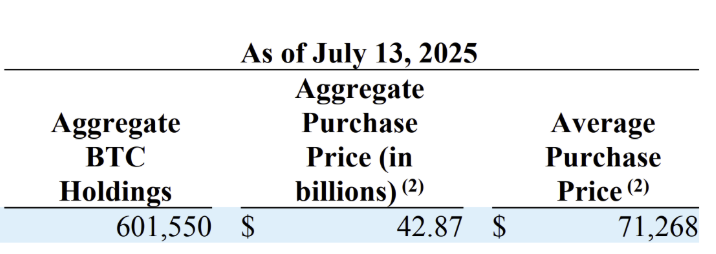

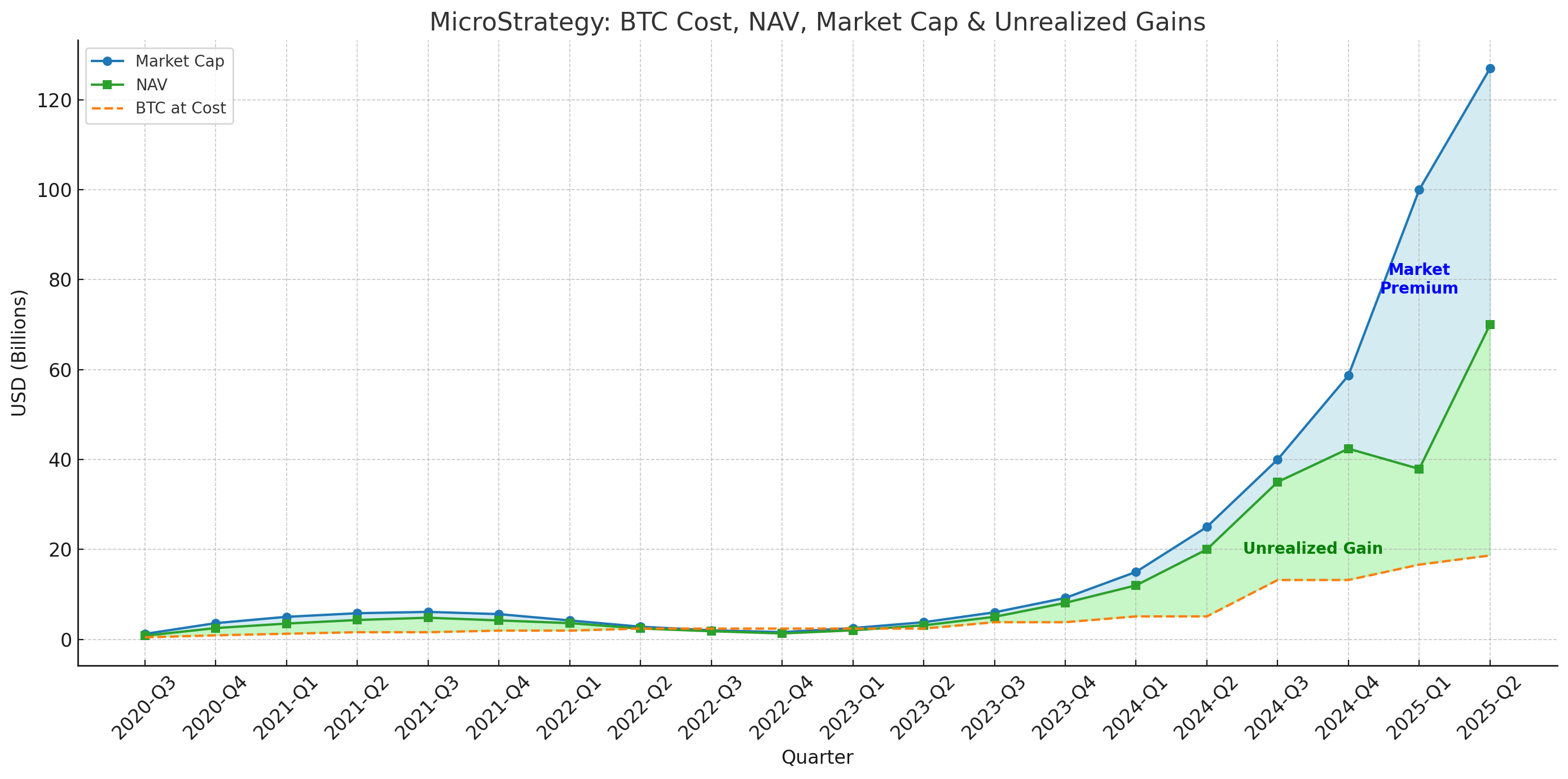

Strategy’s Bitcoin-heavy model echoes the dotcom era: bold bets, speculative inflows, and sky-high valuations. With $30B in unrealized gains and a market cap nearly double its NAV, the company looks less like a business—and more like a leveraged crypto momentum play