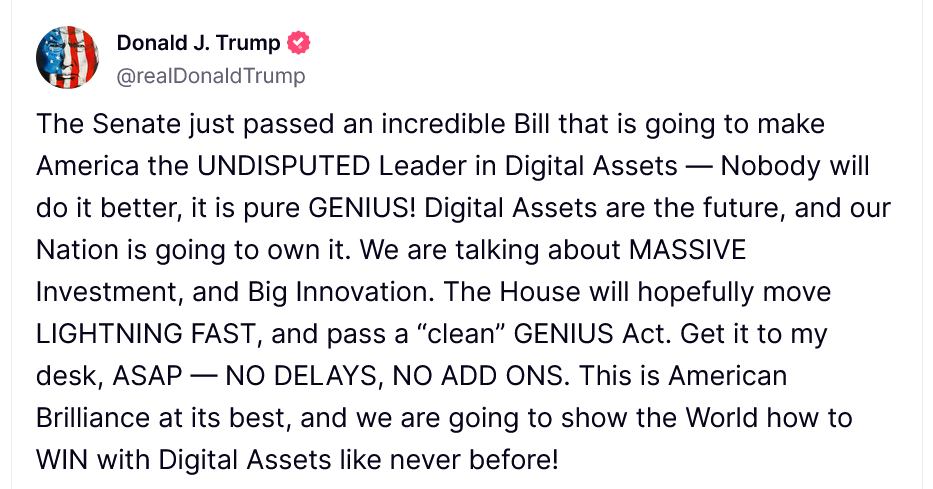

GENIUS Act Clears Senate: U.S. Takes Major Step Toward Stablecoin Regulation

The U.S. Senate has passed the GENIUS Act, a sweeping bill to regulate dollar-backed stablecoins while promoting private-sector leadership in digital finance. Backed by the Trump administration, the bill now heads to the House—marking a pivotal moment in the future of digital dollars.